Steve Monnington, CEO of Mayfield Merger Strategies, reports on an unprecedented time for events M&A.

In last month’s column I analysed the three big PE transactions involving CloserStill Media, Emerald and Questex. However, we weren’t done there. On June 2nd, PE firm Hellman & Friedman announced that they had acquired Hyve for $1.8bn in a transaction that represents the 2nd largest exhibition deal of all time.

Hyve’s transformation pays off

The price paid for Hyve is a testament to the transformation of the business by Mark Shashoua and his team. The former business, originally named ITE, operated 300 (mainly small) shows across Russia, Central Asia, India, Turkey, China and Southeast Asia. Hyve today is a complete reinvention running 33 shows with 18 brands in sectors such as ecommerce, healthcare and health tech, marketing technology and education. It’s focused heavily on Western markets with around 65% to 70% of the business now based in the US.

Traditional trade exhibitions have given way to content and meetings-led events such as ShopTalk, Fintech Meetup and POSSIBLE. In a recent interview with Flashes & Flames, Shashoua said of the pre-arranged meetings “It’s one of the key products we roll out across the portfolio. We run around 200,000 meetings a year within the events themselves. To be clear, these meetings are integrated into the events, not separate from them. They drive around 20% of our profit, but more importantly they drive RoI for customers. That was one of the big shifts we made. We focused heavily on connectivity within events.”

The Trade Show Big Bang

Taken together, the 4 transactions means that, in the space of 4 weeks, over $5.5bn has just been invested by Private Equity in some of the biggest organisers.

- Hyve Group – acquired by Hellman and Friedman for $1.8bn.

- CloserStill Media – acquired for $1.77bn by a new fund from existing owner Providence Equity Partners with Searchlight Capital Partners joining as co-investor.

- Emerald Holding – acquired for $1.5bn by Apollo Funds

- Questex – acquired by Apollo Funds for an undisclosed amount (but presumed to be $400m – $500m). Questex will be merged with Emerald

The Hyve, CloserStill and Emerald transactions are all in the top 4 valuations of all time behind Informa’s £3.8bn acquisition of UBM in early 2018 but it seems that the massive vote of confidence from the investment community in live events is not matched by the UK government. It’s ironic that this level of investment comes at the same time as VisitBritain’s decision to restructure its business events division following reductions in government funding by 41% prompting fears across the meetings and events sector about the future of the UK’s international business events activity and competitiveness. COVID taught us that the government doesn’t really understand the events sector and the economic benefits it brings, but data from the latest Events Industry Council report on the Global Economic Significance of Business Events shows that 70% of exhibitors say face-to-face relationship building is the single hardest thing to replace.

The growing significance of Private Equity in the exhibition sector

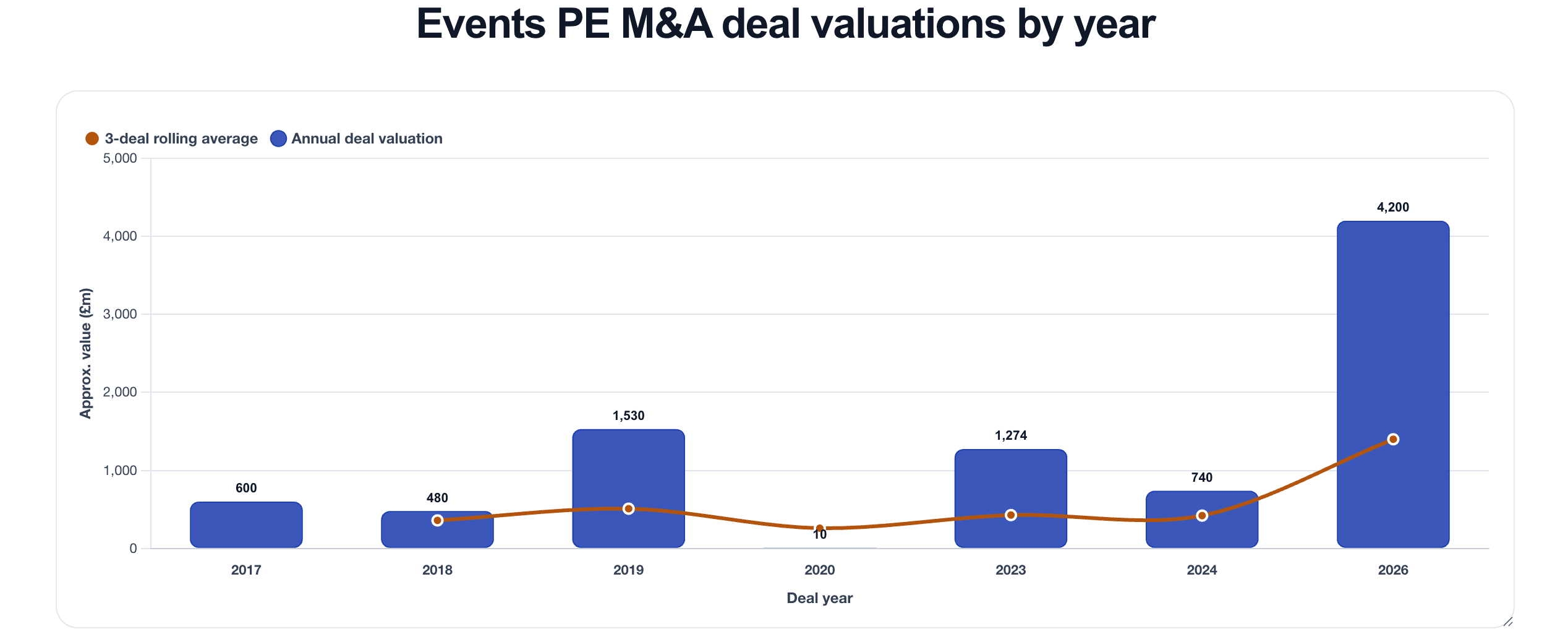

Barış Onay, a London-based B2B events and media entrepreneur and consultant, advising on event strategy, digital transformation, and value creation for organisers has been tracking private equity investment in the exhibition sector. He has analysed 34 transactions starting with HgCapital’s £45m investment in Clarion in October 2004 which facilitated their MBO from Earls Court & Olympia through to this month’s Hyve transaction.

The chart below, covering deal valuations from 2017 to 2026, shows how extraordinary the last month has been, and we are only halfway through 2026.

The theme coming through strongly from Private Equity after the market meltdown at the beginning of February this year is AI related. They are looking at what defensive plays they can make where they are not going to be materially exposed to AI, and events businesses are on that list. Combine this with the tailwinds that AI is bringing to events and we can see why PE are prepared to pay punchy multiples for high growth, high quality event assets.

Doubling down on the sector

The other part of the story is the emerging shift from the traditional private equity time horizons (typically 3 to 5 years) to longer term plays, but Onay has also identified a more nuanced shift in the type of ownership.

“After ownership by NVM, Phoenix, Inflexion and Providence, CloserStill were clearly heading for another flip but the recent transaction broke the pattern. Providence didn’t sell to another PE firm. Instead, Searchlight came in alongside. That’s a co-control recapitalisation, not an exit. Although it’s a different Providence fund, it’s the same PE firm staying in the asset and bringing in Searchlight as a partner, realising the value for the investing fund and then holding for the next leg.”

Onay sees this as a structural shift rather than an isolated transaction and highlights three other transactions that hint at longer term ownership:

Nineteen Group, Sept 2024: Phoenix moved it into a £200m continuation fund (Kline Hill, Ares co-leading) rather than selling. Same logic, keep the platform, recycle capital.

Comexposium, 2018–19: Charterhouse exited not to another PE fund but to Crédit Agricole Assurances. Insurance capital is functionally a buy-and-hold owner.

Easyfairs, 2024: Cobepa (a Belgian holding company, not a closed-end fund) together with Inflexion took shares alongside founder Eric Everard. Long-dated capital, not a flip vehicle.

“Here we have three different mechanisms – continuation funds, insurance balance sheets, and evergreen holdcos – which are all converging on the same thing: keeping good event platforms in the same hands for longer.”

Graphite Capital cashes in on Hanson Wade’s data business

There was more private equity action, somewhat overshadowed by the 4 blockbuster deals, with the sale of Beacon – the clinical trials database owned by Hanson Wade – to Corton Capital. Although not an events transaction, it does have potential event implications. UK private equity firm Graphite Capital originally acquireda majority stake in London-based global conference and information provider Hanson Wade for £95m through a management buyout in August 2019. This was their first investment in the events sector and within 6 months when COVID hit, they saw the portfolio of events they had acquired being systematically cancelled. While the events side of the business stopped, Beacon grew rapidly and over the last four years has accounted for almost all the growth in the business.

The sale of Beacon for an estimated £250m – £300m means that Graphite has already achieved a significant return on their original overall investment and they still own the events businesses which mainly comprise of conferences for the life science, construction (datacenter and construction engineering in the US) and HR sectors. The question now is whether Graphite go for a complete breakup of the business (although there are a lot of small events) or follow the sentiment of the PE firms analysed above and retain, invest, acquire and grow.

Transactions announced since the last column.

| Buyer/Investor | Business | Sector | Country |

| Hellman & Friedman | Hyve | Portfolio | UK/Global |

| Corton Capital | Beacon (Hanson Wade) | Life Sciences | UK |

| Founderpath | SaaStock | Tech | UK/Europe |

| Smartwork Media | JA New York | Jewellery | USA |

| Novi Labs | Gascon | Energy | USA |

| EasyFairs | Xpo Group | Portfolio + Venue | Belgium |

| Messe Stuttgart | Cable & Wire | Industrial | India |

| Nimdzi Insights | Localisation World | Languages | Global |

| KoelnMesse | Amara Expo | Dental, Furniture | Indonesia |

| Retail Global | Power Retail | Retail | Australia |

| AqKva | HavExpo | AquaCulture | Norway |